Stock Alert: engineered for success – a UK innovator born out of the Havana tobacco trade

ALERT 13th January 2022 |

Havana in the 1850s was a place of sun, sea, and… cigars.

Around this time, the Cuban capital was at the heart of the booming tobacco trade. The commodity was becoming increasingly coveted thanks to changes in popular culture.

Cuba’s subtropical climate was (and still is) conducive to widescale tobacco farming, helping to meet the world’s insatiable demand for tobacco.

By 1859, Cuba was home to 10,000 tobacco plantations. Havana alone was home to 1,300 tobacco factories.

Many Cubans flocked to Havana to find work in the industry.

Jose Molins was one of them. He sought to capitalise on the growing craze by opening his very own shop that sold hand-rolled cigars and cigarettes in 1874.

However, he wasn’t satisfied. Molins wanted to find a way to produce cigarettes at scale. Rolling cigarettes one by one was a little tedious after all.

Seeking inspiration, he arrived on English shores in the early 1900s. Close proximity to the tobacco docks of London, another hub of the industry at the time, sounded more like home to him.

Cigarette-making machinery started to appear, as the London-based players sought to keep pace with demand.

Molins desired to create his own cigarette-making machine, but he simply couldn’t afford to.

He had to make do with importing his own cigarette machines from the United States. He sold them on to UK cigarette producers for profit.

Nevertheless, it gave him valuable expertise that he would pass on to his two sons, Harold and Walter.

As they say, the rest is history…

By 1912, Jose had passed away, and the brothers vowed to continue their father’s legacy by forming their own company, Molins Machine Co. Ltd., specialising in cigarette-making machinery.

The company became embroiled in the war effort, assisting in the manufacture of munitions for World Wars I and II.

Although a cloud of distraction, involvement in the war turned out to have a silver lining. It bolstered finances and enabled extensive R&D into new machinery.

This would lead to the birth of a mega cigarette-making machine that the world hadn’t seen before.

It was faster and more robust than other machines and allowed more advanced packaging, such as cellophane wrapping.

Crucially, it received a patent in 1926 which allowed the Molins brothers to establish itself as a global brand to cigarette producers around the world.

And more than a century later, the company continues to exceed expectations in the creation of packaging machinery.

There’s more to packaging than meets the eye…

Therein lies the idea behind our latest Frontier Tech Investor recommendation.

The Molins brothers came up with a better, more efficient way of doing things with their cigarette-making machine.

They knew something others didn’t about the importance of efficient, robust product assembly and packaging.

In particular, packaging is an integral part to successful commercialisation of a product.

It must be tailored to a specific product with absolute precision and practicality.

Failing this, the contents inside may become damaged, reducing product quality and, ultimately, customer satisfaction.

For example, packaging a wine glass in a thin, flimsy plastic wrapper is no good due to its fragility.

In addition, poor packaging could lead to an excess of packaging being used. This can incur unnecessary extra costs to the business and, also, have a damaging environmental impact.

Speed and efficiency are an important aspect too. Is the production line churning out enough products to remain competitive? Is there a threat of machine malfunction that could hamper the supply chain?

And what about how it looks on the eye? The colour, design, the dimensions. Although that’s mainly the prerogative of the brand, it still has to be delivered through the packaging.

It could be the difference between somebody plucking it from the shelves over a close substitute.

Realistically, the only feasible way to achieve all of these aspects in rapid time at the lowest possible cost is through automated machinery.

From the origins of Cuban tobacco machinery to the future of smart, autonomous machinery, this is a company with long-standing roots that’s eyeing up the potential of a market that has the ability to deliver for shareholders.

No doubt, it has been transformed into a company that the Molins family would be proud of.

Introducing your latest Frontier Tech Investor recommendation…

MPAC Group (LSE: MPAC) is your latest Frontier Tech Investor recommendation. MPAC is a provider of packaging and automation solutions to consumers in the pharmaceutical, healthcare and food and beverage industries.

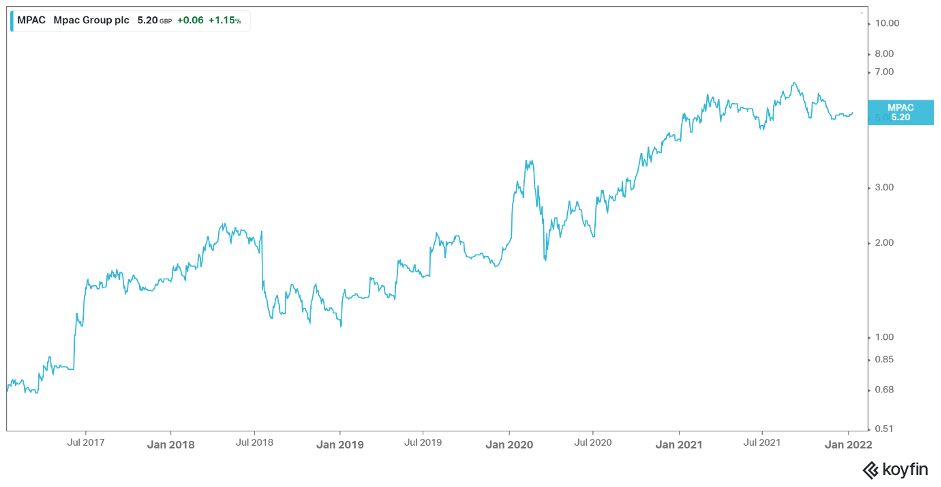

The company is an AIM-listed company on the London Stock Exchange. It has a market cap of £105.9 million and a current share price of 525GBp.

MPAC is based in Tadcaster, UK.

As shown, the company has an illustrious history, spanning more than 100 years. The company officially became MPAC Group in 2018, having previously been listed as Molins Plc.

Prior to this, the company sold off the tobacco machinery division in 2017 to Italian packaging solutions group Coesia S.p.A. This was to focus on producing packaging machinery and technology relevant for industries other than just tobacco and, in doing so, to realise MPAC’s growth potential.

MPAC could be described as an industry leader in providing sustainable packaging solutions.

The company seeks to integrate and streamline the manufacturing processes of its customers. Starting with product assembly, then initial and case packaging and finally, palletisation.

MPAC operates through three subsidiaries: Lambert, Langen and Switchback.

Lambert specialises in full-line solutions (product assembly through to palletisation), whereas Langen and Switchback are mainly focused on packaging.

Of course, such processes require machinery.

MPAC makes expertly engineered machines that help its customers optimise their manufacturing lines.

The picture below shows MPAC’s packaging machinery configuration in full flow.

Source: MPAC Group

Source: MPAC Group

The machines are tailored to the customer’s needs and evolve with their ideas and requirements.

For example, when Covid-19 first reared its ugly head in March 2020, it was a massive curveball for the whole economy.

One of MPAC’s flagship products, the Diablo Midi machine, was chosen by an unnamed healthcare customer to efficiently produce and package coronavirus testing kits.

In a time of urgency, the machine was quickly adapted to the customer’s needs. It enabled them to reach their production target, and at the same time, help in the UK’s fight against the virus.

It’s an extraordinary piece of kit. You can watch it in action here. This segment of “healthcare & other” makes up around 47% of the company sales for the half-year 2021. Pharmaceuticals makes up around 2%.

However, the majority of MPAC’s business (51%) comes from the food and beverage industry.

The company helps deliver efficiency gains in the packaging of pizza, biscuits, frozen foods and craft beers.

For example, one of its customers, an unnamed pizza manufacturer, wanted to increase speed and flexibility of its pizza packing process.

MPAC Langen’s MAESTRO cartoning machine provided the solution. It enabled its customer to package up to 140 pizzas per minute.

MPAC’s machines are installed in a number of global blue-chip conglomerates, including Kraft Heinz Company (NASDAQ: KHC), Unilever (LSE: ULVR) and Abbott Laboratories (NYSE: ABBT).

The machines are optimised so that the overall equipment effectiveness (OEE) is maintained. A hygienic stainless-steel design is a stand-out feature, reducing the chance of dilapidation.

Intelligent machines

Something that sets MPAC apart from its rivals is the use of “smart” technology in its machines.

MPAC leverages the use of intelligent machines. In other words, machines that are programmed to automate tasks and coordinate information to its operator.

This is possible through their MPAC Intelligent Machine Interface (iMi).

The interface proactively provides information about maintenance needs and performance enhancements. At the tap of a few buttons the operator can access this information on their device from anywhere in the world and take appropriate action.

Sensors installed in the machine monitor the environment and machine vibrations. This data is then logged by the system and is sent via the iMi interface to the user.

Instead of the human telling the machine what to do, it’s the machine telling the human what to do.

It allows a new level of productivity to be reached, eliminating human error and making for a more efficient and transparent manufacturing process.

A reality check… of the augmented kind

Another aspect that sets MPAC apart is its customer support services. It has a deep, genuine desire to consistently deliver value to its customers.

Again, its support services utilise state-of-the-art technology.

For example, MPAC uses the Microsoft HoloLens (a type of augmented reality headset) to create a virtual, real-life picture of a customer’s machine. With this, MPAC’s technicians can quickly detect and attend to faults, reducing precious downtime.

Augmented reality is a trend in itself, that is gaining traction around the world as part of the digital transformation spurred by lockdown restrictions. According to Global News Wire, the market is set to increase sixfold between 2020 and 2026, rising from $14.7 billion to $88.4 billion.

This helps to explain why we are excited about MPAC right now.

We think that MPAC’s potential is exciting. It is an innovative, forward-thinking company that is adding extraordinary value to manufacturing lines across a variety of industries. In addition, its ability to harness some of the most ground-breaking technologies of the modern day provide it with a strong competitive advantage.

Also, what makes MPAC perfect to add to our Buy List now is this is a company that is highly profitable, growing and which has a lot of cash on its balance sheet.

Financials, risks and action to take

Looking at its last set of full-year financials, for the year ended 31 December 2020, MPAC recorded revenues of £83.7 million. This was a 5.7% decrease on 2019.

The company attributes this decrease to a pause in growth, induced by the pandemic.

However, what impressed us was MPAC’s ability to generate a profit during this turbulent time.

For 2020, operating profits were £6.5 million. This is down from £7.7 million over the same period in the previous year.

The company is also debt free and has £10.3 million in net cash. Interestingly, according to its website, the company stated it will consider future dividend payments in line with trading performance. Currently, due to current market headwinds, there is no dividend. Of course, we will keep you posted on any update regarding this.

To maintain a healthy profit margin under these circumstances highlights the strength of MPAC’s business.

In part, the healthy figures were driven by MPAC’s fresh expansion into the US market, after the acquisition of Ohio-based packaging company Switchback in September 2020.

Switchback, which focuses on providing recyclable packaging for the craft beer industry, saw increased demand from manufacturers transitioning towards more sustainable production processes.

In fact, revenues from the Americas accounted for more than half of its total revenues across the year, demonstrating the success of the acquisition, considering that it only came three months before year-end.

In light of COP26 climate summit talks, we think Switchback’s affinity for sustainability will make it a stand-out for potential customers.

Note: MPAC expects to release its full-year financials for 2021 on 14 March 2022 which we anticipate to be strong, again reinforcing why now is an opportune time to invest in the stock.

The more up-to-date figures are MPAC’s half-year figures to 30 June 2021.

These are also cause for optimism. For the six months ended 30 June 2021, revenues were up 20% and profits up 50% on the corresponding period in the previous year (2020).

Furthermore, underlying profit (before tax) was a healthy £4.7 million, well up on the £2.5 million from the same period in 2020.

It’s also exciting to know that MPAC Switchback successfully relocated to a showcase facility in the United States on 16 August 2021, which is now MPAC’s US headquarters.

So, there’s a clear international growth story here too – although probably not quite the one that Jose Molins envisaged when he left his homeland all those years ago.

However, it’s important to consider the risks involved with the company.

The main risk the company faces is headwinds from Covid.

If the Covid situation worsens, with the prevalence of old and new variants, consumer confidence may be reduced. This could reduce demand for MPACs’ premium-priced machinery, and limit profitability and business growth.

In addition, supply chain bottle necks could impede growth. Demand and supply imbalances stemming from the pandemic and Brexit regulations has left the UK noticeably short of materials over the past six months.

This includes raw materials, food and energy – all of which are relevant to MPAC’s business model.

However, MPAC mitigates this through its growing international presence. In all, its machines are installed in up to 80 different countries, so the supply chain issues of one particular country is likely to have little impact on the bigger picture.

Finally, although MPAC prides itself on being a sustainable packaging company, the UK government is enforcing tighter restrictions on the use of packaging altogether.

From 2023, the UK government is enforcing an extended producer responsibility scheme (EPR), which will require companies to monitor and ultimately pay for their waste packaging. According to grocer.com, it could cost UK companies £2.7 billion annually from 2023, with food and drinks companies being worse affected.

This in itself could lower demand for packaging altogether (and MPAC’s services), particularly if more governments follow suit and implement new legislation.

Nevertheless, we believe MPAC has strong upside potential. The company is setting the industry standard for industrial packaging, providing extraordinary productivity gains through the use of ground-breaking technology and machinery.

Jose Molins would undoubtedly be proud of what his company has become.

Action to take

MPAC Group is an AIM-listed company on the London Stock Exchange. It has a market cap of £105.9 million and a current share price of 525GBp.

The average volume is around 27,000 per day, which equates to around £138,000 in value. This makes it a relatively illiquid stock in our view.

On recommendation, the price may spike higher. So, please ensure you stick to our buy limits. If it moves above it, it becomes an active hold, and if it moves below, it becomes a buy.

Action to take: Buy MPAC Group (LSE: MPAC), current price 525GBp, buy up to 610GBp. As a reminder, we will being doing away with stop losses altogether from now on, to save us getting stopped out unnecessarily of stocks that have solid long-term potential. So, please ensure to manage risk accordingly, and stay up to date with our advice on any action to take.

Name: MPAC Group

Ticker: MPAC.L

Price as of 13/01/2022: 525 GBp

Market cap: £105.9 million

52-week high/low: 665.4GBp/188GBp

Buy up to: 610GBp

Source: Koyfin

Source: Koyfin

Sam Volkering

Editor, Frontier Tech Investor

Elliott Playle

Junior Analyst, Frontier Tech Investor